“`html

11/05/2025 – 09:39 PM

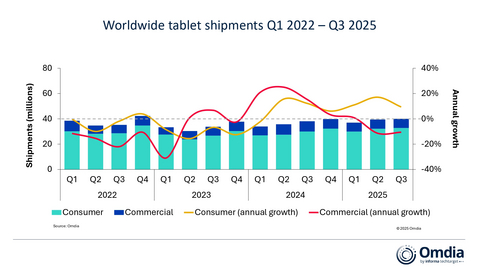

LONDON – The global tablet market continues to defy expectations, posting its seventh consecutive quarter of growth. According to new data from Omdia, worldwide tablet shipments reached 40 million units in Q3 2025, a 5% increase year-over-year. This growth trajectory underscores the enduring appeal of tablets, even as macroeconomic headwinds persist and other consumer electronics segments face softening demand.

Worldwide tablet shipments Q1 2022 – Q3 2025

The driving forces behind this sustained expansion vary across regions. The Middle East and Central Europe saw particularly robust demand, while China maintained its position as a key consumer market. A significant surge in Chrome tablet shipments to Japan, spurred by the government’s GIGA 2.0 education initiative, also contributed substantially to the overall figures. Mirroring this trend, Chromebook shipments reached 4.2 million units, a 3% increase year-over-year, fueled by renewed activity in education deployments worldwide, with Japan once again playing a pivotal role.

Omdia’s analysis suggests a complex interplay of factors at play, including frequent new product introductions that keep consumers engaged, government subsidies that lower the barrier to entry, and a growing appetite for specialized kids’ and gaming tablets. Competitive pricing, strategic promotional campaigns, and the cyclical boost from back-to-school buying further fuel demand.

However, Omdia anticipates a potential slowdown on the horizon. “While Q3 2025 benefited from seasonal sell-in ahead of the holiday period in the West and significant sales events in Asia-Pacific, sell-in is expected to remain muted and largely flat in Q4,” says Omdia Research. “This cautious outlook extends into 2026 as tablet replacement demand is projected to soften. The industry faces the challenge of incentivizing upgrades and finding new use cases to maintain its momentum.”

That challenge includes innovating in hardware to make tablets even more essential to consumers and businesses, according to Omdia. Industry watchers are considering ways to enhance user experience, from improvements to display technology that would reduce eye strain and improve color accuracy to increased processing speeds and more streamlined multi-tasking capabilities that would make them credible laptop alternatives.

Software innovations could also play a key part in helping tablet vendors increase retention and sell upgrades. Enhanced productivity apps, better integration with other devices and platforms, better security, better personalization, and cloud-based services offering seamless data syncing across devices are several areas companies can focus on.

Vendor performance in Q3 2025 painted a varied picture. Apple maintained its dominance with 14.3 million units shipped, holding its own but recording flat growth compared to the previous year. Samsung also posted stable figures, shipping 6.9 million units. Lenovo emerged as a growth leader, shipping 3.7 million units, marking a 23% year-on-year increase driven by the expansion of its commercial tablet business in Europe, the Middle East, and Africa (EMEA). Huawei followed in fourth place with 3.2 million units and 11.5% growth, further solidifying its position despite ongoing geopolitical pressures. Xiaomi rounded out the top five, shipping 2.6 million units with a modest annual increase of 2.3%.

The Chromebook market, while smaller overall, also witnessed notable activity, particularly in the education sector. Lenovo led this segment with 1.4 million units shipped, a substantial jump of 54.6% year-on-year. Acer followed with an 18% market share and global shipments of 0.8 million units. HP ranked third, shipping 0.7 million units. Asus, like Lenovo, benefited from Japan’s GIGA 2.0 project, securing fourth position with an impressive 59% year-on-year growth, while Dell rounded out the top five.

The Chromebook’s reliance on the educational market could prove a vulnerability if investment in remote learning fades, or if it does not branch out into other business uses for the device and operating system.

Note: Unit shipments in thousands. Percentages may not add up to 100% due to rounding.

Source: Omdia PC Horizon Service (sell-in shipments), October 2025

“`

Original article, Author: Jam. If you wish to reprint this article, please indicate the source:https://aicnbc.com/12349.html