“`html

11/10/2025 – 07:45 PM

SSR Mining Inc. (Nasdaq/TSX: SSRM) has released the promising results of its Technical Report Summary (TRS) for the Cripple Creek & Victor Gold Mine (CC&V) in Colorado, revealing a robust economic outlook for the operation. The report, titled the “2025 CC&V TRS,” highlights a significant after-tax Net Present Value (NPV) and extended mine life, underscoring the strategic importance of the CC&V acquisition for SSR Mining.

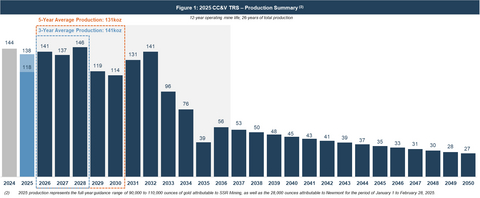

<p style="font-size:85%Figure 1: 2025 CC&V TRS – Production Summary (2): 2025 production represents the full-year guidance range of 90,000 to 110,000 ounces of gold attributable to SSR Mining, as well as the 28,000 ounces attributable to Newmont for the period of January 1 to February 28, 2025.

<p style="font-size:85%Figure 1: 2025 CC&V TRS – Production Summary (2): 2025 production represents the full-year guidance range of 90,000 to 110,000 ounces of gold attributable to SSR Mining, as well as the 28,000 ounces attributable to Newmont for the period of January 1 to February 28, 2025.

The TRS paints a picture of a highly profitable asset, especially as gold prices remain elevated and inflationary pressures persist, potentially squeezing margins for less efficient operations. The current projections provide a strong foundation for SSR Mining’s future cash flow generation.

- The after-tax NPV5% stands at $824 million, calculated using consensus gold prices averaging $3,240 per ounce over the mine’s lifespan. Importantly, the NPV demonstrates significant leverage to gold prices, increasing to approximately $1.5 billion at a $4,000 per ounce gold price. This sensitivity highlights the potential for upside should gold market fundamentals continue to support higher prices.

- The mine is projected to have a 12-year operational life, translating to 26 years of total production supported by 2.8 million ounces of gold in Mineral Reserves.

-

In the near term, from 2026 to 2028, CC&V is expected to produce an average of 141,000 ounces of gold annually. This sustained production rate should generate a substantial boost to SSR Mining’s financials and contribute to the company’s strategic growth initiatives.

- Over the same three-year period, annual after-tax operating cash flow and free cash flow are projected to average $196 million and $128 million, respectively, based on consensus gold prices. At a higher gold price of $4,000 per ounce, these figures would increase to $235 million and $168 million, respectively. This free cash flow further strengthens SSR Mining’s capital deployment strategy and its ability to enhance shareholder value.

- Beyond current reserves, CC&V possesses substantial exploration upside. Measured & Indicated Mineral Resources, exclusive of Mineral Reserves, total 4.8 million ounces of gold, with an additional 2.0 million ounces classified as Inferred Mineral Resources. The gold prices used in the calculation of CC&V Mineral Reserves and Mineral Resources are $1,700/oz and $2,000/oz, respectively, unchanged from the prior statement as of December 31, 2024. This resource base offers significant opportunities for future expansion and the extension of the mine life.

- The acquisition of CC&V has an exceptional implied after-tax transaction Internal Rate of Return (IRR) in excess of 100%. This is based on the initial $100 million cash payment made in February 2025, upcoming contingent payments, and realized mine site after-tax free cash flow, plus TRS free cash flow projections. This robust IRR emphasizes the strategic and financial soundness of the transaction for SSR Mining.

Rod Antal, Executive Chairman of SSR Mining, commented on the successful integration of CC&V, noting that the initial acquisition price of $100 million was already recovered in mine-site after-tax free cash flow. Antal further emphasized the operation’s growth potential, citing the substantial Mineral Resource base.

The TRS, effective July 1, 2025, will soon be accessible on both the company’s website and the U.S. Securities and Exchange Commission (SEC) website as part of a Current Report on Form 8-K. This provides investors with complete transparency into the assumptions, methodologies, and risks underpinning the valuation of the CC&V mine.

| Table 1: CC&V TRS Highlights at Consensus Gold Prices | |||

|

Three-Year Profile | Five-Year Profile | ||

| Unit | 2026 – 2028 | 2026 – 2030 | |

| Total Gold Production | Au koz | 424 | 657 |

| Average Annual Gold Production | Au koz | 141 | 131 |

| Total Operating Cash Flow (GAAP) | $M | $587 | $761 |

| Total Capital Costs (GAAP) (3) | $M | $203 | $283 |

| Total Free Cash Flow (non-GAAP) (4) | $M | $384 | $478 |

| Average Annual Free Cash Flow | $M | $128 | $96 |

| Cost of Sales (GAAP) | $/oz sold | $1,799 | $1,901 |

| Cash Costs (non-GAAP) (4) | $/oz sold | $1,800 | $1,902 |

| All-In Sustaining Costs (non-GAAP) (4) | $/oz sold | $2,051 | $2,135 |

(3) Total capital costs include sustaining capital, development capital, and reclamation. |

|||

|

(4) The Company reports non-GAAP financial measures including after-tax free cash flow and All-In Sustaining Cost (“AISC”) per ounce sold (a common measure in the mining industry), to manage and evaluate its operating performance at its mines. All cash flow figures are presented after tax. Free cash flow is calculated as operating cash flow less capital costs. AISC include costs associated with non-cash inventory movements. See “Cautionary Note Regarding Non-GAAP Financial Measures” for an explanation of Cash Costs and AISC and a reconciliation of these financial measures to the most comparable GAAP financial measures. |

|||

| Table 2: 2025 CC&V TRS – After-Tax NPV Sensitivity | |||||

| LOM Gold Prices | $/oz | $2,754 | Base Case (5) | $3,726 | $4,212 |

| Sensitivity | % | -15% | — | +15% | +30% |

| NPV5% | $M | $340 | $824 | $1,299 | $1,767 |

|

(5) Base Case gold price assumption averages $3,433/oz from 2025 to 2030 and $3,094/oz for the remainder of the mine life. |

|||||

CC&V has demonstrated strong operational and financial performance since SSR Mining gained control. As of September 30, 2025, the mine had generated approximately $115 million in after-tax free cash flow, placing it on track to reach the upper range of its attributable 2025 output guidance of 90,000 to 110,000 ounces. Including the $100 million initial cash payment and $175 million in future contingent payments, realised free cash flow, coupled with the life of mine projections, the CC&V acquisition is expected to provide SSR Mining with a highly impressive IRR in excess of 100%.

The performance and future projections for the Cripple Creek & Victor Gold Mine point towards a valuable and lucrative addition to SSR Mining’s portfolio. The extended mine life, strong cash flow, impressive return on investment, and resource expansion potential suggest that SSR Mining is well-positioned to keep benefitting from this acquisition for years to come.

CC&V Mineral Reserves and Mineral Resources (“MRMR”) (7)

| (7) Please see “Supplemental Mineral Reserve and Mineral Resource Information” at the end of this press release for additional details. Mineral Resources are exclusive of Mineral Reserves. Numbers may not add due to rounding. | |||

|

Table 3: SSR Mining CC&V MRMR as of July 1, 2025 |

|||

| (100% attributable) | Tonnes (kt) | Grade (g/t) | Gold (koz) |

| Total P+P Reserves | 235,134 | 0.37 | 2,814 |

| M&I Mineral Resources | 344,844 | 0.44 | 4,845 |

| Inferred Mineral Resources | 149,603 | 0.41 | 1,966 |

| Table 4: 2025 CC&V TRS – Operating Metrics Summary | ||

| Unit | Life of Mine | |

| Total Material Mined | Mt | 373 |

| Average Daily Mining Rate | ktpd | 85 |

| Total Ore Mined | Mt | 226 |

| Total Waste Mined | Mt | 146 |

| Strip Ratio | W:O | 0.65 |

| Total Ore Stacked | Mt | 226 |

| Average Daily Stacking Rate | ktpd | 52 |

| Ore Grade Stacked | g/t Au | 0.39 |

| Contained Gold Stacked | koz | 2,832 |

| Gold Recovery | % | 51.6 |

| SSRM | Proven | Probable | Proven + Probable | Metallurgical | ||||||||||||

| Gold | Country | Share | Tonnage | Au Grade | Gold | Tonnage | Au Grade | Gold | ||||||||