“`html

China’s online retail market surged in the first half of 2025, fueled by a potent mix of pro-consumption policies, evolving consumer preferences, and a supply-side eager to adapt. From personalized experiences to a renewed focus on health, and seamless online-offline integration, the landscape is ripe with both challenges and opportunities. According to a recent report by e-commerce data analytics firm Shangzhizhen, these trends are reshaping how Chinese consumers spend their money online.

Key findings from the report:

Government initiatives and e-commerce “billion-yuan subsidy” campaigns have created a powerful demand-pull effect, particularly in the electronics and appliances sectors. Sales of mobile phones and accessories jumped 32.6% year-over-year in the first six months of 2025, with JD.com maintaining its market dominance, capturing over half of all sales. Major appliance categories, including refrigerators, washing machines, and televisions, all experienced positive sales growth. The booming e-sports industry is driving demand for gaming laptops, smartphones, and ergonomic chairs.

Consumer spending is increasingly driven by specific demographics. The “new elderly” (ages 50-75) prioritize quality-of-life goods, leading to a surge in targeted products such as senior-focused food, healthcare, and apparel. Meanwhile, Gen Z views consumption as a form of self-expression, fueling growth in areas like the “Gu-Zi economy” (collectible figurines and merchandise) which cater to their need for emotional fulfillment.

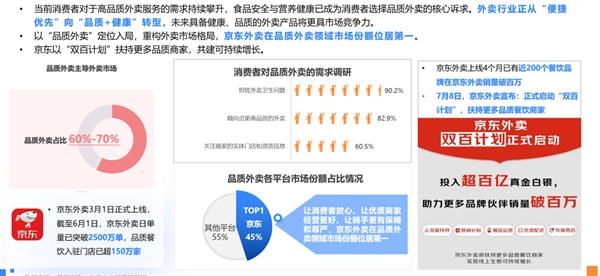

A distinct “M-shaped” consumption pattern is emerging, where consumers simultaneously seek value-for-money everyday items and are willing to pay a premium for high-end and design-forward products. Preferences are also shifting toward finer, healthier, and more personalized experiences. AI-powered innovation is enabling appliances and digital devices to evolve towards “scenario-based intelligence + personalized experience”. First-to-market products are generating buzz, with new releases across numerous categories outpacing the overall category growth. Major e-commerce players are actively connecting with foreign trade enterprises, optimizing “dual circulation” supply chains. The combination of online and offline commerce continues to energize the market, immediate retail helps the reovery of physical locations, with JD’s newly launched food delivery service taking the top spot in just four short months with a substantial 45% share, and around 200 restaurant brands each generating over a million in sales.

Policy Boost Propels Electronics Growth: Mobile Accessories Surge Over 30%

The combined effect of government stimulus packages and e-commerce promotional events has significantly boosted online retail performance. These policies are strategically designed to steer consumption towards green, intelligent, and high-quality products.

In the electronics and appliances sector, the impact has been particularly pronounced. Government incentives to replace old appliances with energy-efficient and smart alternatives have spurred the market. The report identifies that mobile phone and accessory sales grew 32.6% between January-June, with JD.com controlling a significant portion of sales. Refrigerator, washing machine and television sales also enjoyed strong growth, validating the potency of these policy interventions.

The e-sports sector has also blossomed thanks to clear government support. The state council released specific plans to promote consumer spending on gaming (including e-sports and surrounding products). Cities like Beijing, Shanghai, Guangzhou, and Hangzhou have followed by introducing similar measures which include e-sports in the development of a new economy and culture, which has directly driven the demand for gaming laptops and smartphones. This not only drives hardware spending, but confirms China’s commitment to evolving beyond sub-culture into the mainstream, with supporting product development, reflecting the digital lifestyle preferences of GenZ and the state’s commitment to the digital culture.

Young and Old Drive Consumer Market Innovation: 260 Million Gen-Z Drive Approximately 40% of Spending

Current consumer market drive is shifting from product-based drive to segment-based motivations, especially with “old” and “young” sectors.

Because there is an evolving “aging” demographic, the elderly are receiving higher education, accumulating wealth and increasing health awareness. No longer wanting only basic goods, the aged are pursuing lifestyle upgrades, socialization, and self-actualization. Especially the “new elderly” (50-75 age-range), healthy and independent, they harbor both the desire and capability to spend, composing a high-quality and emerging market.

Reports indicate a tourism increase of 58% for the 61-65 age range between January and September of 2024. 2025 data shows tourism is above 40% compared to previous years. Additionally, the first half of the year saw elderly furniture, clothing, senior products, and network retail increase dramatically.

Approximately 260 million Gen-Z individuals contribute 40% of all spending, with figurine and badge collecting driving much of the market. This has produced a market value nearing 170 billion yuan, up more than 40% in 2024. Consumer behavior is viewed as self-expression, emotional fulfillment, identity confirmation, curiosity, and self-cure for many.

Value and Quality Dominate Consumer Mindsets: Structure Shows Distinct ‘M Shape’

Current research indicates consumers’ consumer values are becoming more diverse. Refined, individualized, and health-centric priorities fuel consumer pursuits.

A People’s Forum research report showed that nearly 60% view their consumer behavior as carefully-thought-out, where high quality is matched by compatible pricing. Industry products such as Hebei Baigou bags, Ningxia Tanyang, and Zhuji socks each exceeded network retail growth by over 20%. On JD’s 618 event, the plan “Factory product subsidy” drove a lot of sales, including 10 million paper products, 8 million cookware products, and 3.6 million clothing orders.

On the other hand, sales have shown a distinct “M shape” model. Consumers are seeking both high-quality daily products (0-500yuan phones, 0-100yuan clothing orders), but also luxury-level products (10000+ yuan phones, 2000+ yuan clothing). JD’s 618 event showed 3x growth in laptops, 100%+ growths in phone and appliances. These met much of the consumer expectations.

Consumer health awareness has contributed to growth, with 76.9% seeking stronger body habits. Sales have increased in nutrition, health monitoring equipment, massage, and therapy equipment (30%+). JD’s shopping day saw Ejiao, bird’s nest, and slimming aids show 200%+ increase in sales.

With fast-living considerations, there is an increased demand for instant fulfillment. Reports indicate that first half of 2025 saw floral products online climb 80%, 50% for wooden bracelet products, 40% in creative housing. Outdoor products are also showing promise.

Innovation Propels Industrial Upgrade: AI Enables Unlikely Consumer Growth

Supply-side innovators are responding to demand. Artificial intelligence is driving product iteration, and empowers AI powered appliances through products from Dreame, Haier, and Midea, evolving toward “scenario-based intelligence + personalized experience”. First half of the year saw 130% increase in AI notebook sales, 200% AI wearable, and 330% AI smartphone sales. Retailers are also getting in on the AI efforts, which helps reshape the new ecology. JD created a new digital spokesperson and helped sellers generate content for their products.

First-to-market products draw traffic, and show “first launch” benefits. The first have of 2025 new skincare products and clothing rates surpassed those of general categories. On the JD shopping event, digital product sales volumes grew nearly 4x, home goods 7x, and exclusive product orders jumping 18x.

Instant Retail Propels Commerce Recovery: Seller and Consumer Approve JD Food Delivery

Sellers and companies are innovating to propel retail and forecast a 2 trillion RMB instant retail economy by 2030. First half of the year saw retail giants JD, Meituan, and Taobao focus on instant retail to aid commerce recovery.

Reports show JD food had 45% of the market share only 4 months after launch, and about 200 food vendors enjoyed million dollar sales. Luckin, Cotti, and Mixue all experienced 100 million level sales, and many others broke 10 million in sales. JD 7Fresh increased speed and shopping experience, and broke records during holidays.

Consumer holidays are still powerful, but skew toward personalization and luxury. Spring Festival, Valentine’s Day, Mother’s day, and Dragon Boat sales were significant for luxury items. New trends like rental car driving showed growth, with 85% rented outside of normal areas, and a 24% consumer increase. Pet travel arrangements have also increased in demand in recent times.

First-half data has shown significant consumer potential in retail while rapidly evolving to a more personalized and intelligent experience. Understanding and exploiting these changes will be the key to sustained growth.

“`

Original article, Author: Tobias. If you wish to reprint this article, please indicate the source:https://aicnbc.com/5061.html